By Marcia Le Roux,

Business Development Manager, Africa.

Efficiency in digital transformation within the general insurance industry enables insurers to reduce costs, improve customer experience, increase agility, leverage data for decision-making, and enhance collaboration with external stakeholders.

These factors contribute to competitive advantage and long-term success in an increasingly digital and customer-centric landscape.

Inefficiencies in these factors have greater consequences in how an insurer –

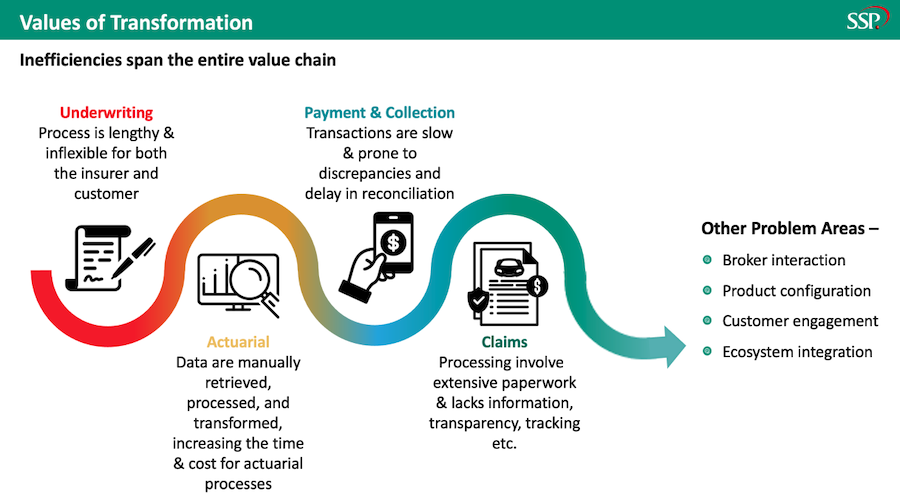

- Communicates with the broker

- Configures products

- Manages customers and

- Integrates their business ecosystem

These are some of the areas where inefficiency has an impact:

Underwriting

Leveraging a convergence of data, technology, and human capital could transform underwriting inefficiencies into a multiplied value creation. Driven by the need for efficiency and evolving customer expectations, most insurers have been moving steadily toward greater digitisation. Underwriting has been a key focus area: Most insurers have actively been upgrading their underwriting capabilities with more advanced technology and expanded data sources.

Actuarial

Fragmented data with an inaccessible legacy system prevents insurance companies from drawing out the value and making data work through actions. Under the current IFRS 17 requirements, it is also more important to access relevant and easy data to retrieve and provide reports to comply with these audit requirements.

Payment and collections

Insurances are going digital to mitigate a slow and delayed transaction process. Many insurers already accept inbound premium payments from policyholders. Now, outbound claims payments are also catching on. These changes will bring benefits to both insurance companies and insurance customers with the goal of creating a convenient, intuitive, and seamless user experience.

But there are still challenges to face, such as a fragmented customer experience (when using a third-party vendor for digital payments, for example, a fragmented customer experience is possible), a complex integration path, limited resources for an insurance company to develop a digital payment system in-house; security and compliance (especially these days, when data breaches and cyberattacks have become commonplace); and lastly a platform to support multiple payment methods.

Claims

Offering multiple payment methods for premium and claims payments is convenient for policyholders, but it can complicate things for the insurance company. Accounts need to be reconciled, and any discrepancies found and resolved quickly.

To lessen the impact of legacy issues, it is important to have a digital system that offers real-time data, line-item detail, and aggregated reconciliation that makes analysing payment activity and reconciling accounts quick and easy.

Ultimately, inefficiencies in these four areas have far-reaching consequences, influencing how insurers interact with brokers, configure products, engage with customers, and integrate within the broader ecosystem.

Embracing digital transformation and addressing these inefficiencies is pivotal to thriving in the evolving insurance landscape.

Marcia Le Roux

Business Development Manager, Africa.

Watch Marcia's talk below